Navigating the Supply Collapse and the “Forced Seller” Vintage of 2026

Originally published by Arie van Gemeren, CFA

Adapted and formatted for the StellarVest Insights Blog

“The best time to plant a tree was twenty years ago. The second-best time is now. The worst time is when everyone else has already planted theirs, and you’re competing for sunlight.”

The investment window for real estate is open.

Not cracked.

Not slightly ajar.

Open.

And I don’t say that as a promotional line. I say it because the last 18 months have produced one of the most important convergences we’ve seen in years:

- Supply collapse

- Distress

- Capital paralysis

The last time this exact configuration appeared, the investors who acted quietly and patiently built some of the best real estate vintages of a generation. Most people will miss this one too. This piece explains why — and what to do about it.

Part I: Three Converging Signals

A buying window never announces itself clearly. As the old economist joke goes:

If two economists pass a dollar bill on the street, they’ll both assume it can’t be real because someone else would have already picked it up.

Real estate windows work the same way.

The best opportunities often appear when sentiment is weakest, capital is frozen, and most market participants are too psychologically exhausted to move. In my view, today’s opportunity is being created by three distinct signals converging at once.

Signal 1: Supply Collapse in Supply-Constrained Markets

New multifamily construction in Portland has fallen to multi-decade lows.

Apartment completions in 2025 reportedly came in roughly 54% below 2024 levels — not a slowdown, but a collapse.

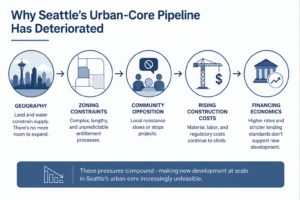

Seattle’s urban-core pipeline has similarly deteriorated under the pressure of:

- geography,

- zoning constraints,

- community opposition,

- rising construction costs,

- and financing economics that no longer support new development at scale.

Nationally, Cushman & Wakefield’s Q1 2025 Multifamily MarketBeat pointed to the shrinking construction pipeline as the “light at the end of the tunnel,” with new starts declining sharply while absorption improved year-over-year.

The Pacific Northwest is simply the clearest expression of a broader structural trend.

And importantly:

This is not temporary softness.

This is structural supply compression.

You cannot build more waterfront.

You cannot create more mountain-constrained infill neighborhoods.

You cannot replicate decades of employment density overnight.

The supply moat is real. That matters because replacement cost now sits dramatically above acquisition pricing in many infill markets.

The Math

Approximate replacement cost for new multifamily construction in Portland today:

- $350–450 per square foot

Pricing on older vintage assets in desirable infill neighborhoods:

- $150–200 per square foot

That is a massive disconnect.

Critics often argue that replacement cost alone should not determine value because new buildings are theoretically superior assets.

Fair point.

But replacement cost matters because it creates defensibility.

If your basis is dramatically below what it costs to build a new product, you gain:

- greater resilience during rent pressure,

- stronger downside protection,

- and flexibility that competitors cannot easily replicate.

The supply math itself creates a margin of safety.

More importantly, supply collapse combined with a stable or rising population typically leads to:

- upward rent pressure,

- NOI growth,

- and improving investor appetite over time

Signal 2: Forced Sellers — The 2019–2021 Reckoning

From 2019 through 2021, a generation of value-add operators aggressively deployed capital into Sunbelt markets including:

- Phoenix

- Austin

- Charlotte

- Atlanta

The assumptions were familiar:

- 3% cap rates

- floating-rate bridge debt

- 7% annual rent growth

- short hold periods

- compressed exit caps

Then the environment changed.

Rates moved dramatically higher.

Debt costs exploded.

Supply surged in many Sunbelt markets.

Rent growth slowed or reversed.

Cap rates expanded.

The arithmetic broke.

By 2025, the consequences had become difficult to ignore:

- Many 2019–2021 vintages materially underperformed projections

- Sponsors began quietly managing extensions and capital calls

- Distress accelerated across portions of the value-add landscape

- Some operators began handing assets back to lenders

The pricing data reflects the reset. Apartment values nationally remain well below their 2022 peak, according to several major indexes. These are not orderly repositionings. These are the consequences of floating-rate leverage colliding with one of the fastest rate increases in decades. And that distinction matters.

These sellers are not opportunistic sellers.

They are not rebalancing portfolios.

They are solving liquidity problems.

Historically, forced sellers create the foundation of major real estate buying windows.

They do not care about your investment thesis.

They care about survival.

That dynamic creates opportunity for patient buyers with disciplined capital structures and long-term time horizons.

Consider the Imperial Arms in Portland as a practical example:

- acquired at a going-in cap rate above 7%,

- at a significant discount to replacement cost,

- during a period of deeply negative market sentiment.

That is often how great vintages are built.

Signal 3: Capital Paralysis

The third ingredient is equally important.

The institutional capital that normally competes aggressively during recovery periods remains largely frozen.

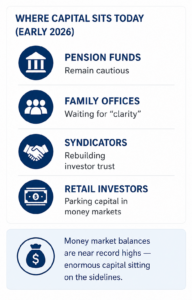

Today:

- pension funds remain cautious,

- family offices are waiting for “clarity,”

- syndicators are rebuilding investor trust,

- and retail investors continue parking capital in money markets.

As of early 2026, money market balances reportedly sit near record highs. That is enormous capital sitting on the sidelines waiting for certainty.

But buying windows rarely offer certainty. They offer discomfort. That discomfort is precisely why opportunity exists. The best moments to acquire real estate are usually not periods of easy capital and universal optimism.

They are periods where:

- capital is fearful,

- transaction activity slows,

- and competition temporarily disappears.

And importantly: Transaction activity itself may already be quietly improving before sentiment catches up.

That is often an early-cycle signal.

Part II: The Historical Fingerprints

Every major real estate buying window shares four common characteristics:

- Supply contraction

- Distress or forced selling

- Frozen capital markets

- Widespread pessimism

Those fingerprints appeared during:

- the Resolution Trust Corporation (RTC) era of the early 1990s,

- the post-GFC recovery period from 2009–2012,

- and several other major cyclical resets.

The pattern is familiar.

By the time the “all-clear” arrives publicly, pricing has usually already recovered.

The best opportunities occur while uncertainty still dominates headlines.

Part III: The Mathematics of the Window

See this practical underwriting framework for current acquisitions.

Example Framework

Assume:

- Acquisition pricing around $150/sf

- Replacement cost above $400/sf

- Going-in cap rates around 6.5–7.5%

- Fixed-rate debt in the 6–6.5% range

- Conservative 5-year hold period

- Moderate annual rent growth assumptions

If supply remains constrained while rents normalize gradually over time:

- NOI compounds steadily,

- exit cap rates potentially compress,

- and replacement-cost advantages create structural downside protection.

The important point is not aggressive underwriting.

It is that the math can still work even under relatively conservative assumptions.

That is usually a sign of a strong vintage environment.

Part IV: Why Most Investors Still Won’t Move

One of the strongest sections in the piece is the explanation for why many investors remain inactive despite improving long-term conditions.

1. Recency Bias

The pain of 2021–2023 remains fresh. Investors burned by floating-rate leverage, capital calls, or underperforming vintages are psychologically hesitant to re-enter. Cycle damage takes time to heal.

2. Contrarian Positioning Is Emotionally Difficult

Buying in markets with negative headlines requires separating structural fundamentals from short-term sentiment. Most investors struggle to do that consistently.

3. Cash Feels Safe

Money market yields have given investors a psychologically comfortable alternative to risk assets. But those yields are temporary. Real assets with durable cash flow and supply constraints often become more attractive as short-term yields compress.

4. Buying Windows Rarely Feel Comfortable

This may be the most important point. Great buying windows almost always feel risky while they are occurring. If they felt obvious, pricing would already reflect the opportunity.

Part V: The Playbook

We will close with a practical framework for investors evaluating the current cycle.

Find the Supply Moat First

Focus on markets where supply cannot easily flood the system.

Examples include:

- coastal cities,

- land-constrained metros,

- infill neighborhoods,

- mountain-constrained markets,

- and areas with durable demand anchors.

Buy Below Replacement Cost

This creates structural downside protection that financial engineering cannot replicate.

Use Conservative Debt Structures

Floating-rate bridge debt paired with long-duration investment theses proved catastrophic for many operators during the last cycle.

Debt structure matters.

Underwrite for Patience

Conservative leverage.

Longer hold periods.

Operational durability.

The best vintages are often created by investors capable of holding through volatility rather than relying on perfect timing.

Lead With Downside in Investor Conversations

In today’s environment, sophisticated investors often care more about “What happens if you’re wrong?” than optimistic return projections.

That mindset shift matters.

What to Avoid

Be warned against confusing “cheap” with “opportunity.”

Distress alone is not the thesis.

The real question is whether the underlying market has durable structural advantages.

Markets with:

- unlimited supply,

- weak demand anchors,

- easy entitlement,

- and chronic overbuilding risk

may simply be resetting into another cycle of oversupply.

The Bottom Line

Nobody knows exactly when this window closes.

But the three defining conditions behind it:

- supply collapse,

- forced sellers,

- and capital paralysis

will not persist forever.

Eventually:

- money market capital will rotate back into real assets,

- distressed inventory will clear,

- transaction markets will normalize,

- and replacement-cost discounts will narrow.

By the time consensus becomes comfortable again, the opportunity will likely already be repriced.

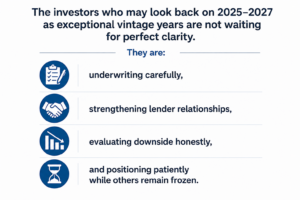

The investors who may look back on 2025–2027 as exceptional vintage years are not waiting for perfect clarity.

They are:

- underwriting carefully,

- strengthening lender relationships,

- evaluating downside honestly,

- and positioning patiently while others remain frozen.

That has historically been how durable real estate wealth is built.