Charles Ponzi’s Second Act — and What Today’s Investors Should Learn From It

Introduction

History rarely repeats itself exactly — but financial cycles often rhyme with remarkable precision. The story of Florida’s 1920s land boom is often remembered as a colorful period of speculation, excess, glamour, and eventual collapse. But beneath the mythology sits a much more important lesson for investors and operators today: the distinction between a paper market and a use-value market. That distinction matters now just as much as it did in 1925. What follows is not simply a history lesson. It is a case study in how speculative markets form, how leverage and momentum distort pricing, how narratives overpower fundamentals, and how seemingly unstoppable booms unwind far earlier than most participants recognize.

The mechanics may evolve from generation to generation. The structure rarely does.

Jacksonville, September 1925

Charles Ponzi stepped off a Seaboard Air Line passenger car in Jacksonville with one suitcase, a new business card, and a federal conviction five years behind him. He had already become infamous for the 1920 Boston fraud scheme that permanently attached his name to an entire category of financial crime. He had served three and a half years in prison, been released, re-indicted on state charges, skipped bail, and arrived in Florida as a technical fugitive.

- He had almost no money left.

- No business.

- No credibility in the Northeast.

- What he did have was timing.

Because by late 1925, Florida had become the center of the most feverish real estate speculation in America.

Newspapers across the country were filled with stories about:

- Coral Gables lots doubling in value within months

- Miami Beach developments selling out before infrastructure existed

- Addison Mizner’s Spanish-style mansions rising across Boca Raton

- Young brokers becoming wealthy almost overnight

- Palm trees, sunshine, luxury, and easy money

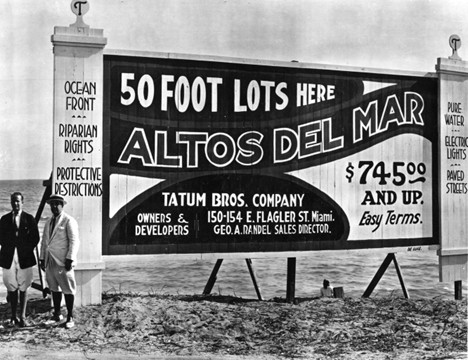

The “Sunshine State” had become a national obsession. Within weeks of arriving, Ponzi incorporated the Charpon Land Syndicate, rented office space, and began selling 23-acre tracts of supposedly “prime West Palm Beach” land to out-of-state investors. The economics were staggering.

He was selling the land at roughly twenty-three times his acquisition cost. Much of the land was swamp. Some of it was not even properly titled property. Yet investors bought anyway. Hundreds of lots were sold before authorities arrested him.

And this is the key point most histories overlook: By 1925, the legal Florida land market looked structurally similar to what Ponzi himself was doing.

That is what makes the story important.

Ponzi was not operating outside the psychology of the market. In many ways, he was simply amplifying it.

What Florida Had Become

In 1920, Florida was still largely undeveloped.

It had fewer than one million residents — less than Baltimore at the time — and its economy revolved primarily around:

- citrus,

- lumber,

- cattle,

- and seasonal tourism.

Five years later, the state had been transformed.

Several powerful forces collided simultaneously:

Postwar Wealth Expansion

The Northeast and Midwest had accumulated substantial wealth after World War I. Investors and families suddenly had discretionary capital available for speculation and second-home ownership.

Automobile Accessibility

The rise of automobile travel changed everything. With the Dixie Highway connecting northern states to Florida, middle-class Americans could now physically reach the state for the first time in meaningful numbers.

Favorable Tax Policy

The Revenue Act of 1921 reduced capital gains taxes, increasing the attractiveness of speculative investing.

Health Migration Narratives

Tuberculosis remained a major health threat in America, and warm climates were marketed as medically beneficial. Florida aggressively sold itself as restorative paradise.

National Advertising Campaigns

The marketing was relentless.

By 1924, full-page advertisements promoting Florida developments appeared regularly in:

- The New York Times

- Chicago Tribune

- Boston Globe

- Philadelphia Inquirer

Developer Carl Fisher reportedly spent the equivalent of nearly $18 million annually in today’s dollars promoting Miami Beach alone. He installed giant Times Square billboards showing palm trees against snowy cityscapes. He staged elaborate publicity events. Florida was no longer simply a destination — it became a national aspiration.

The numbers reflected the frenzy:

- Florida’s population grew approximately 60% between 1920 and 1925

- Miami’s population increased roughly fivefold

- Land prices in some counties rose more than ten times in three years

At peak speculation, an estimated 60% of Miami’s working-age population either held or had applied for a real estate broker’s license.

That statistic alone tells the story.

When nearly everyone becomes financially dependent on transaction volume continuing indefinitely, caution disappears from the system.

The Financial Instrument That Fueled the Boom: The Binder

Every speculative cycle eventually creates a financial structure that accelerates momentum beyond economic reality. In 1925 Florida, that structure was called the binder. The mechanics were simple — and extraordinarily dangerous.

A buyer would place 10% down on a property. That deposit secured control of the lot for approximately 30 days. During those 30 days, the buyer had two options:

- Close on the property by paying the remaining balance

- Sell the binder contract itself to another buyer at a higher price

The key detail:

The actual property often never changed hands.

The paper did.

This created one of the most efficient speculative flipping mechanisms in real estate history. A buyer with $5,000 could temporarily control a $50,000 property. If prices increased 20% in a week — which was not uncommon at the peak — the binder itself could be sold for a massive profit before the original purchaser ever took title.

At the height of the boom:

- binders changed hands multiple times within weeks,

- lots traded repeatedly without site visits,

- and many participants had no intention of owning or developing the land at all.

The market was no longer pricing land based on utility, cash flow, or end-user demand. It was pricing the assumption of a future buyer. That distinction matters enormously.

The Binder Boys

The market developed its own culture and ecosystem. The so-called “binder boys” became symbols of the era — young commission-driven brokers working the streets of Miami in linen suits, flipping paper contracts for immediate cash commissions. Transactions moved so quickly that commissions were frequently paid in cash because banking systems could not process deals fast enough.

By 1925, Miami alone accounted for an astonishing share of total U.S. real estate transaction volume. At one point, estimates suggested Miami represented nearly 20% of all real estate transaction activity in the country despite having a relatively tiny permanent population base.

Even more striking:

An estimated 90% of transactions were speculative resales, not end-user ownership transactions.

That is the definition of a paper market.

The Peak of the Boom

The summer of 1925 represented the euphoric peak. And like many peaks in hindsight, it did not feel dangerous at the time.

There was no universal skepticism.

No widespread caution.

No consensus expectation of collapse.

The cautious participants had largely already exited the conversation months earlier after being priced out by aggressive speculation. The dominant voices were the people whose livelihoods depended on momentum continuing. Entire developments were being sold before roads, utilities, or infrastructure existed.

New boom towns emerged almost overnight:

- Hollywood

- Opa-Locka

- Hialeah

- Miami Shores

Out-of-state banks aggressively financed speculative purchases, often using Florida binders themselves as collateral for additional loans. The leverage embedded in the system became extraordinary. And importantly, the stock market itself was not the center of speculation at this stage. The hottest money had already migrated into real estate.

This becomes one of the most important structural observations in the entire story:

Real estate frequently leads broader financial cycles rather than lagging them.

The First Cracks Appear

The initial break in the boom did not come from regulators or fraud investigations. It came from logistics. By late 1925, the rail systems supplying South Florida became overwhelmed. Construction materials could no longer move efficiently into the region.

- Lumber shipments stalled.

- Building supplies backed up.

- Projects slowed dramatically.

The Florida East Coast Railway and Seaboard Air Line eventually restricted incoming freight shipments.

At the time, this looked temporary. In reality, it exposed the fragility of the speculative structure underneath the market. Because the arithmetic of the binder market assumed projects would continue progressing indefinitely. If construction slowed, buyers suddenly faced the possibility of closing on properties that could not realistically be developed for months or years.

That changed behavior quickly.

By early 1926:

- transaction volume had fallen sharply,

- speculative flipping slowed,

- and forced closings began increasing.

The market was already weakening before the national narrative changed.

The Great Miami Hurricane

Then came September 1926. The Great Miami Hurricane struck as a Category 4 storm with estimated sustained winds near 140 miles per hour.

The physical destruction was catastrophic:

- more than 25,000 homes destroyed,

- major flooding across Miami Beach,

- infrastructure devastation,

- widespread fatalities,

- and enormous economic disruption.

But the hurricane itself was not the sole cause of the collapse. That is the most misunderstood part of the story. The speculative structure was already weakening before the storm arrived.

The hurricane simply revealed how fragile the system had become. Once outside capital stopped flowing into Florida, the paper market collapsed rapidly.

The sequence unfolded in stages:

Stage One: Binder Defaults

Speculators unable to resell contracts forfeited deposits and abandoned positions.

Stage Two: Developer Insolvencies

Developers relying on continuous inflows of new speculative capital suddenly lost liquidity. Major firms collapsed.

Stage Three: Bank Failures

Banks heavily exposed to Florida real estate paper began failing throughout 1927 and 1928.

Stage Four: Municipal Bond Defaults

Boom-town infrastructure had been financed through debt tied to continued growth assumptions. As growth stalled, municipalities defaulted.

Stage Five: The 1928 Okeechobee Hurricane

Another devastating hurricane further destroyed confidence and accelerated economic decline.

By early 1928, Florida was already in a severe real estate depression. And remarkably: The broader stock market would continue climbing for more than a year afterward.

The Three-Year Head Start

This is one of the most important lessons in the entire piece. Florida real estate was already collapsing while the stock market was still rising toward its 1929 peak. The Dow Jones would not peak until September 1929 — nearly two years after Florida’s speculative unwind had begun.

This was not coincidence. It was sequencing.

Capital first flowed aggressively into real estate speculation. When Florida broke, that capital rotated back into equities, helping fuel the final stock market melt-up before the Great Depression. The lesson is uncomfortable for investors: Real estate cycles often break before financial markets acknowledge underlying economic stress. Operators on the ground frequently see deterioration earlier than national headlines or market indexes reflect.

The Core Structural Lesson

The most important distinction in the piece is the difference between a paper market and a use-value market. A paper market is dominated primarily by speculative resale activity.

A use-value market is anchored by durable economics:

- actual occupancy,

- long-term demand,

- sustainable cash flow,

- realistic underwriting,

- and operational fundamentals.

Paper markets can appear stable for long periods because continued capital inflow masks structural fragility. But once inflows slow, the lack of true use-value pricing becomes visible very quickly. The structure matters more than the trigger. The trigger simply determines timing.

Modern Echoes

The author draws direct parallels between Florida 1925 and several modern speculative cycles:

- 1999 fiber and dot-com infrastructure speculation

- 2005–2007 subprime mortgage markets

- 2020–2022 Sunbelt multifamily value-add syndication cycles

Each cycle had different assets and different financial instruments. But the underlying structure remained remarkably similar:

- rapid transaction velocity,

- compressed hold periods,

- dependence on new capital inflows,

- narrative-driven pricing,

- and growing detachment from underlying cash flow fundamentals.

The Six Indicators of a Paper Market

The framework presented in the original piece identifies six recurring warning signs.

1. Transaction Volume Outpaces Population Growth

When transaction activity grows far faster than actual demographic demand.

2. Hold Periods Collapse

Assets become priced primarily for resale rather than long-term ownership or operations.

3. Explosive Growth in Intermediaries

Brokers, syndicators, and transaction facilitators multiply faster than underlying economic activity.

4. Dependence on Recently Arrived Capital

Pricing becomes dependent on continued inflows from newer market participants.

5. Narrative Premiums Detached from Cash Flow

Stories and future expectations begin dominating operational economics.

6. Tail Risks Are Ignored

Markets stop properly pricing known risks like insurance, climate exposure, refinancing pressure, or regulation.

The framework is not intended as a prediction tool. It is a structural diagnostic.

Final Thought

Charles Ponzi’s Florida land venture is often treated as a historical side story. In reality, it became a near-perfect miniature of the broader market psychology surrounding him.

The lesson is not simply about fraud. It is about structure. Markets do not collapse merely because optimism exists. They collapse when pricing becomes detached from durable economic utility and increasingly dependent on continuous inflows of speculative capital. That distinction matters in every cycle. And it always will.

Source: “The Great Florida Land Boom: Charles Ponzi’s Second Act, and How to Avoid the Next Housing Bubble” by Arie van Gemeren, CFA (Apr. 24, 2026).