How a Timeless Strategy Became Toxic

Phoenix, AZ – October 2021.

“Syndicator” (an amalgamation of the man, not a real person) stands in front of a 200-unit garden apartment complex. The property is being sold at a 3.2% cap rate. The debt is a floating-rate bridge. 3.5%, interest-only. The business plan assumes 7% annual rent growth over 5 years and an exit at a 4% cap rate. With a healthy assumption that population growth will continue unabated, and of course, that supply won’t change at all. He wires the money. His investors cheer. He posts about it on Instagram.

Phoenix, AZ – October 2024.

That same syndicator stares at a capital call notice. Rents are down. The loan has repriced to 8%. The property can’t cover its debt. The 2021 equity is gone – vaporized. He’s on the verge of handing the keys back to the lender. He doesn’t post online about this. This is NOT a story about a bad operator.

This is a story about what happens when a timeless strategy collides with a perfect storm of cheap money, financial engineering, and social media amplification.

________________________________________

In the Beginning …

Value-add real estate, at its basic level, is a fairly sensible approach to building wealth in real assets. You buy an underperforming property, improve it, and harvest the gains. We all do it, to an extent. Even home flippers are playing “value-add”. They are acquiring a distressed or run-down home and “sprucing” it up. It’s literally a tale as old as real estate. I remember my dad telling me, as a kid, about a fabled “real estate guy” who bought one property, improved it, then sold it and used the proceeds to buy two. So on so forth. And today the man has fifty properties (or some such number – it doesn’t matter, the point was the growth story)!

It’s like the real estate American Dream.

The key thing is – it was a patient game. You found a building that was mismanaged or physically tired. You fixed it. You raised rents to market. You held. The strategy worked because it was grounded in intrinsic value creation. You were actually making something better. Not hoping for cap rate compression. Not betting on interest rates. Not relying on financial engineering.

Then something changed.

Between 2010 and 2022, value-add real estate transformed from a conservative improvement strategy into a speculative, leverage-dependent machine that systematically destroyed capital when the cycle turned. We should all be asking: What the heck happened?

The answer to this isn’t as simple as you would think. The common refrain (and I’ve said it) is that cheap debt = disaster. True by the way. But the setup for the Value-Add mania of 2010 – 2023 is multivariate. These things always are. And it’s a convergence of events that I can say – without hyperbole – is mostly unprecedented in human history.

________________________________________

Era I: Patient Improvement (1950s–1980s)

Now, value-add wasn’t always a pithy, fun, social-media amplified phrase. There was a time (pre-gold standard breaking) when it was just a normal, everyday strategy that made sense. Let’s dig into the era that came before. The foundation, if you will.

I should add that the post-WWII decades weren’t a monolith. They contained multiple distinct monetary regimes, and each had different implications for real estate investors.

________________________________________

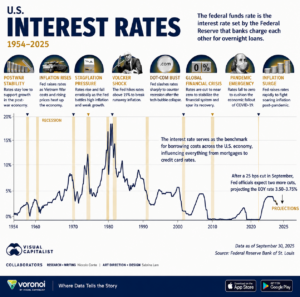

1950–1971: The Bretton Woods Constraint

From the end of World War II until Nixon closed the gold window, the dollar was pegged to gold at $35 per ounce. This was a genuine constraint on credit creation. The money supply couldn’t expand endlessly because there was an anchor. Real rates were positive and stable. Speculation existed, but it operated within limits. You couldn’t borrow your way to infinite returns because the monetary system itself imposed discipline.

Real estate investors in this era bought buildings, improved them modestly, and held for income. The strategy was fundamentally defensive. Returns came from NOI growth, not financial engineering.

________________________________________

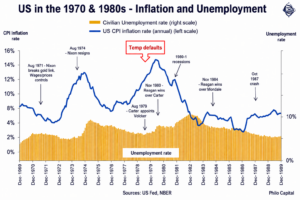

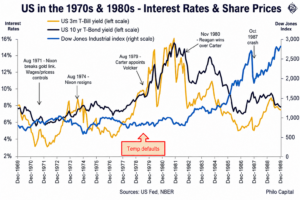

1971–1979: The Post-Nixon Shock

When Nixon severed the dollar’s link to gold, the constraint disappeared. Arthur Burns at the Fed kept rates artificially low under political pressure. Inflation ran 6–12%+ through much of the decade. Real rates were often negative.

This was an easy money period. So why didn’t we see the same toxicity that emerged in the 2010s?

Because the infrastructure to weaponize cheap money didn’t exist. There were no institutional fund structures with deployment pressure and fee incentives. No bridge loan products designed for quick flips. No CMBS securitization machine. And perhaps most critically – since at its core all finance is a narrative game – there was no social media amplifying get-rich-quick narratives to millions of retail investors.

Cheap money without the machinery to deploy it aggressively at scale produces inflation. But it doesn’t produce a value-add bubble.

________________________________________

1979–1980s: The Volcker Discipline

Then Volcker arrived. Rates hit 20%. Real rates went massively positive. The easy money era ended violently.

This enforced genuine conservatism. You couldn’t play games with leverage when debt cost 15%. The math simply didn’t work. Real estate investing returned to fundamentals: buy at a discount, improve operations, hold for income.

Which, by the way, discounts abounded all the way through to the early 1990s. This era featured both the crushing pain of the Volcker Rates and the S&L Crisis as well. And both presented great opportunities for genuinely strong buys.

Key insight: The “patient improvement” era wasn’t defined by any single factor. It was the absence of the convergence that would later create toxicity. Hard money constraints (1950s–1971). Lack of financial infrastructure (throughout). Volcker discipline (late 1970s onward). Any one of these was sufficient to keep the strategy grounded.

The toxicity required all the barriers to be removed simultaneously.

________________________________________

Era II: Institutional Scaling (1990s–2000s)

The 1990s saw the beginning of the machinery being built.

The savings and loan crisis created a wave of distressed assets. Institutional capital, such as pension funds, endowments, and insurance companies, entered the real estate market in force. Value-add strategies scaled from individual building plays to portfolio-level aggregation.

Interest rates began their long secular decline. The Fed Funds rate fell from 8% in 1990 to roughly 1% by 2003. This enabled more leverage, but risk controls remained in place. NCREIF data shows value-add returns averaged 10–12% annually through this period, outperforming core strategies by 2–4%. The outperformance came from active management – operational improvements, better leasing, modest renovations.

But this era also introduced the seeds of future problems:

Fund structures with deployment pressure.

When you raise a $500 million fund, you need to deploy that capital. You can’t return it to investors because you couldn’t find good deals. The structure creates an incentive to buy, even when the market is frothy. And since you are NOT a long-term holder by design, you’re optimizng for financially engineered returns, producing high promote, and getting out of the deal fast enough to turn a profit.

Fee structures misaligned with outcomes.

Management fees on committed capital. Acquisition fees at closing. Sponsors got paid to deploy, and then paid on IRR (which is itself a time-weighted metric), which reinforces a “flip” mentality.

Securitization and financial engineering.

CMBS emerged. Debt became a product to be manufactured and sold, not a relationship to be maintained. This enabled leverage at scale. Contemplate that before the emergence of securitization you often dealt with “relationship” lending instead, where the lender was forced to deal with the results of their loan. While not perfect (as the S&L Crisis and many other banking crises showed), it did enforce some discipline.

The toxicity system was being built.

But cheap money wasn’t yet chronic, and one crucial amplifier was still missing: the ability to broadcast the narrative to millions of retail investors in real-time.

Era III: The ‘Perfect’ Storm (2010s–2020s)

The Global Financial Crisis ought to have been a cleansing of the animal spirits that were restless and awakening in global real estate. But instead, it became the catalyst for the most dangerous convergence in real estate history.

Central banks responded to 2008 with zero-interest-rate policies that lasted, in various forms, for over a decade. The Fed Funds rate sat near zero from 2009 to 2015, rose briefly, then crashed back to zero in 2020. But cheap money alone doesn’t explain what happened. The 1970s had negative real rates, too.

What made the 2010s different was the convergence of every amplifier simultaneously:

1. Chronic ZIRP (Zero Interest Rate Policy)

Not a brief period of easy money, but a decade-plus of near-zero rates. Long enough for an entire generation of investors to believe this was the permanent state of the world. Long enough for business models to be built entirely on cheap debt.

2. Institutional Deployment Machines at Full Scale

By 2010, the fund structure had fully metastasized. Hundreds of billions in institutional capital with mandates to deploy into value-add strategies. Fee structures that rewarded deployment regardless of outcome. Managers who had to buy or return capital.

3. Sophisticated Financial Engineering Tools

Bridge loans with 3-year terms. Floating-rate SOFR products. Interest-only periods designed for quick flips. High-LTV structures that maximized leverage. These tools didn’t exist in the 1970s. By 2015, they were standard.

4. A Mature Securitization Infrastructure

CMBS conduits. Warehouse lines. Debt that could be originated, packaged, and sold off within months. This severed the feedback loop between lender and borrower. The originator didn’t care if the loan performed – they’d already sold it.

5. Social Media Amplification

This is the factor that doesn’t get discussed enough.

BiggerPockets. YouTube gurus. Instagram wealth porn. Real estate TikTok. For the first time in history, investment narratives could spread to millions of retail investors instantaneously. You could watch someone “succeed” in real-time, 24/7.

This created information cascades at a scale never before possible. When everyone sees everyone else “winning,” the pressure to participate becomes overwhelming. FOMO becomes a market force.

6. The “Everyman” BRRRR Narrative

Buy, Rehab, Rent, Refinance, Repeat.

The narrative was seductive: you don’t need capital. You don’t need experience. Just use OPM (other people’s money) and repeat infinitely. Scale to infinite wealth.

This brought massive amounts of unsophisticated capital into the market—retail investors, first-time syndicators, anyone with a laptop and a dream. All chasing the same “value-add” playbook. All competing for the same deals. All driving prices up and returns down.

Here’s an interesting meta-analysis of the use of BRRR across Twitter/X by Grok. While not perfect, you can absolutely see that the term peaked in use from 2019 – 2023, which is fascinating as that’s the period that coincided with the lowest interest rate point.

7. Herding at Unprecedented Velocity

Put it all together and you get herding behavior at internet speed. Sunbelt multifamily became the consensus trade. Everyone knew it. Everyone was doing it. The podcasts said so. The Instagram accounts confirmed it. The fund managers couldn’t afford to miss it.

Cap rates compressed to 3%. Operators underwrote 7% annual rent growth because that’s what the trailing data showed. Floating-rate bridge debt seemed safe because rates had been low for a decade. This was the perfect storm. Cheap money. Deployment machines. Financial engineering tools. Securitization infrastructure. Social media amplification. A viral narrative. Herding at scale.

The 1970s had easy money. The 2010s had all of it, simultaneously. That’s why the outcome was different.

The Unwind

When the Fed raised rates in 2022, it didn’t just increase borrowing costs. It broke every assumption the 2010s value-add machine was built on.

Cap rates expanded from 5% to 7% in many markets—a 19% peak-to-trough decline in asset values. Bridge loans repriced from 3.5% to 8%. Rent growth stalled or went negative in oversupplied markets. Properties that appeared to cash flow suddenly couldn’t cover their debt.

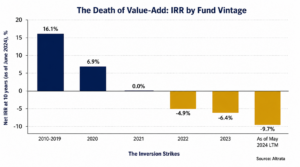

The data on vintage performance tells the story with brutal clarity. The INREV/ANREV/NCREIF Global IRR Index—the industry standard measure of closed-end fund performance—tracks value-add and opportunistic funds by vintage year. The numbers for recent vintages are both disappointing and actually negative.1

• 2021 vintage funds: -5.74% IRR (as of Q4 2024)

• 2019 vintage funds: -6.64% IRR (as of Q1 2025)

• Post-2019 vintages overall: ranged from -6.93% to -10.67% through 2024

These are not low returns. These are losses. Investors in these vintages have, on average, less money than they started with.

For contrast, consider what good vintage timing looks like: the 2008–2010 vintage funds—those that deployed capital into the post-GFC distress—delivered an 18.18% IRR, the best-performing cohort across all regions. The pattern is clear. Capital deployed at the peak of cheap money destroyed wealth. Capital deployed into distress created it.

Academic research confirms this isn’t an anomaly. Li and Riddiough’s 2023 study, “Persistently Poor Performance in Private Equity Real Estate,” found that real estate funds generated negative alphas overall, with performance deteriorating significantly in later vintages—a pattern specific to real estate and not observed in buyout or venture capital funds.

The social media gurus went quiet. The Instagram posts stopped. The podcasts pivoted to “what went wrong” episodes.

But the buildings are still there. They just have the wrong capital structure.

________________________________________

The Return to Fundamentals

The Second Owner Advantage

Every cycle of value-add destruction creates opportunity for patient capital.

The overleveraged syndicators who bought in 2021 are now liquidating their portfolios—often at 30–40% discounts to their basis. The buildings themselves didn’t become worthless. They just have the wrong capital structure.

• Marcus Licinius Crassus, the wealthiest man in Roman history, built his fortune by buying buildings after fires. He’d show up with his private fire brigade, offer to buy the burning property for a pittance, and then put out the fire. The building’s value didn’t change. Only the ownership did.

• Sam Zell did the same thing in the 1970s and 1990s, buying distressed assets from overleveraged operators during credit crunches.

The playbook is timeless:

1. Wait for overleveraged operators to fail

2. Acquire their assets at a discount

3. Recapitalize with conservative debt

4. Hold for the recovery

The 2025–2027 vintage will likely be among the best in decades—not because the buildings are different, but because the sellers are desperate and the social media hype machine has moved on.

Now I say all this with a bit of a wink. Because you know, as well as I do, that buying distressed is the way to go. The trick is to actually do it. To time it right. I had a neighbor back in the day (this was 2016 and onwards) who refused to buy his home. He was a renter. And he didn’t like home prices. And he kept waiting. Waiting. Waiting.

He has missed out on a veritable fortune in that time. To the detriment of him and his family.

What Actually Creates Value

If we strip away the financial engineering, what does real value-add look like?

Physical improvements that increase NOI. This means renovations that tenants will pay more for: updated kitchens, modern finishes, better common areas, improved amenities. The test is simple: Will tenants pay $50–$100 more per month for this improvement? If not, don’t do it.

Operational improvements. Expense reduction, better maintenance practices, improved collections, stronger lease enforcement. This is the unsexy work of actually running a building well. It doesn’t require leverage. It doesn’t require cap rate compression. It just requires competence.

Lease-up and stabilization. Buying a building at 80% occupancy and getting it to 95% is real value creation. You’re not relying on the market. You’re relying on execution.

Repositioning. Sometimes a building is serving the wrong tenant base or positioned incorrectly in its market. Thoughtful repositioning—changing the unit mix, improving the tenant profile, adding services—can create substantial value.

None of this requires cheap debt. None of it requires cap rate compression. None of it requires Instagram followers. All of it creates durable income that survives rate shocks.

________________________________________

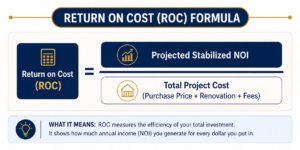

The Math of Value Creation: Return on Cost (ROC)

In a world of 7% bridge loans, you can no longer rely on cheap debt to hide a bad deal. You must understand your Return on Cost (ROC). Also known as your Yield on Cost.

This number is the unlevered yield you earn once all the work is done and the building is leased up. Think of it as your “manufactured” cap rate.

The Two Critical Mathematical Guardrails

To know if a value-add project is a “go” or a “no-go,” your ROC must clear two specific hurdles:

1. The Development Spread: To justify the risk of construction, leasing, and general execution, your ROC should be 150 to 300 basis points (1.5% to 3.0%) higher than the market cap rate for a comparable, already-stabilized building. If Class A buildings are trading at a 5% cap, but your renovation only gets you to a 6% ROC, you are taking a massive risk for a tiny 1% premium. You’d be better off buying the stabilized building and sleeping at night.

2. Accretive vs. Dilutive Debt: This is where most operators are currently dying. Your debt is only accretive (it helps you) if the yield on your renovation is higher than the interest rate on your loan.

- The Math: If you spend $10,000 to renovate a unit and it raises the rent by $100/month ($1,200/year), your Renovation ROC is 12%.

- The Decision: If your bridge loan costs 7%, that debt is accretive because 12% > 7%. But if your renovation only yields an 8% return and your debt is 9%, every dollar you borrow is actually diluting your returns. You are effectively paying the bank more to borrow the money than the renovation itself is producing in new income.

As should be abundantly clear, when you were buying at a 4 cap, financing at 4%, and increasing rents by say $100 – 125 per month, you were getting very little return for your risk.

But you were getting returns, nonetheless, because the rate regime had been very steady for over a decade, so you could eke out minuscule value-add upside on a renovation and it still worked.

Until it didn’t.

________________________________________

Five Rules for Value-Add That Actually Work

1. Buy at a Discount to Replacement Cost

This is your margin of safety. If you can’t build the same building for less than you’re paying, you’re speculating on appreciation. We target 30–40% discounts to replacement cost on every deal.

2. Fixed-Rate Debt Only

Floating-rate debt is speculation on interest rates. You might win. You might lose. But it’s a bet. Fixed-rate debt removes the variable. You know your cost of capital for the entire hold period.

3. Underwrite to Current Income

Pro forma projections are fantasies. Underwrite to what the building produces today. Any improvement is upside—not the base case.

4. Operate as If There’s No Exit

If you had to hold this building for 20 years, would you still buy it? If the answer is no, don’t buy it. The exit market is a gift, not a guarantee.

5. Ignore the Consensus

When everyone is buying Sunbelt multifamily, look elsewhere. When the podcasts are hyping a market, the alpha is already gone.

The best opportunities exist precisely where the crowd isn’t looking

_______________________________________

The Timeless Principle

Value-add real estate was never supposed to be complicated.

Buy buildings that need work. Do the work. Collect higher rents. Hold for cash flow.

That’s it.

The toxicity came when a perfect storm converged.

That convergence may never repeat in exactly the same form. But some version of it will. Because humans don’t change. The greed. The FOMO. The desire to believe that this time is different.

The operators who remember that value-add is about patient improvement—not financial engineering—will build wealth through the next cycle.

The operators who wait for the next perfect storm to ride will get destroyed by it.

The wheel turns ever onward.

Think Well. Act Wisely. Build Something Timeless.

________________________________________